Delivering more actionable and strategically valuable research, The Business Research Company’s 2026 market reports feature market attractiveness analysis, total addressable market evaluation, company benchmarking matrices, interactive Excel dashboards, expanded supply chain intelligence, emerging startup coverage, and detailed product insights.

Aerospace and Defense Additive Manufacturing Market Size, Value And Growth Trends Through 2030

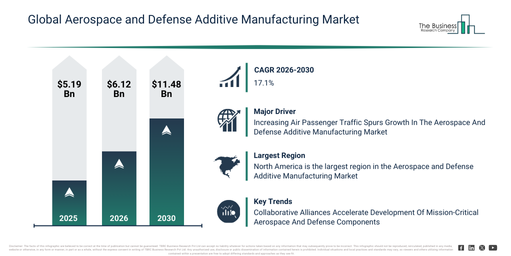

The aerospace and defense additive manufacturing market has experienced rapid expansion recently. It is projected to increase from $5.19 billion in 2025 to $6.12 billion in 2026, indicating a compound annual growth rate (CAGR) of 17.8%. The growth observed in previous periods can be attributed to the early adoption of additive manufacturing for rapid prototyping in aerospace and defense programs, a growing need for complex geometries in radio frequency hardware and propulsion components, the initial integration of powder bed fusion and material extrusion techniques into defense manufacturing workflows, an increasing demand for lightweight and high-performance engine components, and the development of additive methods for repairing and replacing mission-critical parts in military systems.

The aerospace and defense additive manufacturing market size is projected to experience swift expansion over the coming years. This market is predicted to reach $11.48 billion by 2030, demonstrating a compound annual growth rate (CAGR) of 17.1%. Factors contributing to this growth during the forecast period include the increasing application of directed energy deposition and binder jetting for substantial defense components, the rising integration of additive manufacturing to bolster supply chain resilience within aerospace and defense sectors, the heightened fabrication of advanced heat exchangers and casting patterns through additive methods, the escalating requirement for certified 3D-printed propulsion and engine parts to boost platform efficiency, and ongoing advancements in multi-material and high-temperature additive processes that support future defense applications. Key trends anticipated during the forecast period encompass sophisticated multi-material printing for essential aerospace components, a surge in the adoption of additive technologies for quick prototyping, an increase in additive repair and refurbishment activities for defense components, a growing need for lightweight, high-strength engine and structural parts, and the broadening of certified additive manufacturing processes to meet aerospace compliance standards.

Download A Free Sample Report For Comprehensive Market Insights:

Aerospace and Defense Additive Manufacturing Market Development Factors: Which Trends Are Supporting Demand?

The expanding air passenger traffic is anticipated to propel the growth of the aerospace and defense additive manufacturing market. Air passenger traffic measures the total number of individuals boarding commercial flights within a specified period. The adoption of aerospace and defense additive manufacturing technologies can positively influence air passenger traffic by improving aircraft efficiency, driving innovation, enhancing fuel efficiency, and increasing affordability, simultaneously upholding the reliability and sustainability of air travel operations. For example, according to Eurostat, a Luxembourg-based government agency, in December 2025, the number of passengers transported by air increased by 19.3% in 2023 compared to 2022. Thus, the increasing air passenger traffic is a significant factor driving the expansion of the aerospace and defense additive manufacturing market.

Aerospace and Defense Additive Manufacturing Market Segments: Where Are The Largest Growth Opportunities?

The aerospace and defense additive manufacturing market covered in this report is segmented –

1) By Technology: Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Stereolithography (SLA), Selective Laser Sintering (SLS), Other Technologies

2) By Material: Metal, Plastic, Rubber, Other Materials

3) By Platform: Aviation, Defense, Space

4) By Application: Engine Component, Space Component, Structural Component, Defense Equipment, Other Application

Subsegments:

1) By Direct Metal Laser Sintering (DMLS): Titanium Alloys, Aluminum Alloys, Stainless Steel

2) By Fused Deposition Modeling (FDM): Thermoplastic Materials, Composite Filaments

3) By Continuous Liquid Interface Production (CLIP): Resin-Based Materials, Elastomers

4) By Stereolithography (SLA): Standard Resins, Engineering Resins, Bio-Compatible Resins

5) By Selective Laser Sintering (SLS): Nylon Powder, Metal Powders, Composite Powders

6) By Other Technologies: Electron Beam Melting (EBM), Laminated Object Manufacturing (LOM), Binder Jetting

Aerospace and Defense Additive Manufacturing Market Transformation Trends: Which Innovations Are Driving Change?

Key companies operating within the aerospace and defense additive manufacturing market are engaging in strategic partnerships to push forward the creation of vital components for military and aerospace applications. These strategic alliances in the market combine technical proficiency and specialized manufacturing resources, which aids in developing high-performance, mission-critical components and enhances scalability for aerospace and defense uses. Such collaborations support the manufacturing and qualification of advanced metal additive manufacturing solutions, especially for military flight hardware. For instance, in June 2025, Velo3D, Inc., a US-based metal additive manufacturing company, entered a Cooperative Research and Development Agreement (CRADA) with two Naval Air Systems Command (NAVAIR) federal laboratories, the Naval Air Warfare Center Aircraft Division (NAWCAD) and Fleet Readiness Center East (FRC East). Through this collaboration, Velo3D and NAVAIR aim to strengthen additive manufacturing capabilities for aerospace and defense applications by integrating Velo3D’s sophisticated 3D printing technology with NAVAIR’s technical expertise and operational requirements.

Aerospace and Defense Additive Manufacturing Market Major Participants And Competitive Dynamics

Major companies operating in the aerospace and defense additive manufacturing market are General Electric Company, Raytheon Technologies Corporation, The Boeing Company, Lockheed Martin Corporation, Airbus SE, Northrop Grumman Corporation, BAE Systems, Safran SA, Rolls-Royce Holdings, Honeywell Aerospace, Siemens Digital Industries Software, OC Oerlikon Corporation AG, Moog Inc., Aerojet Rocketdyne Holdings Inc., Carpenter Technology Corporation, Renishaw plc, GKN Aerospace, Stratasys Ltd., EOS GmbH, 3D Systems Corporation, Proto Labs Inc., Materialise NV, Desktop Metal Inc., SLM Solutions Group AG, Optomec Inc., Sintavia, Additive Industries, Optisys LLC, CRP Technology SRL, BeAM Machines Inc.

Access The Complete Aerospace and Defense Additive Manufacturing Market Report:

Aerospace and Defense Additive Manufacturing Market Regional Distribution: Which Areas Drive Market Expansion?

North America was the largest region in the aerospace and defense additive manufacturing market in 2025. The regions covered in the aerospace and defense additive manufacturing market report are Asia-Pacific, South East Asia, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Access a Customized Aerospace and Defense Additive Manufacturing Market Report for Deeper Competitive Insights

https://www.thebusinessresearchcompany.com/customise?id=25199&type=smp

Get in touch with us:

The Business Research Company: https://www.thebusinessresearchcompany.com/

Americas: +1 310-496-7795

Asia: +44 7882 955267 & +91 8897263534

Europe: +44 7882 955267

Email us at: marketing@tbrc.info

Follow us on:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

Wasay has over a decade of experience in market research, data modelling, and analytics, with prior experience at GlobalData and Decision Tree Consulting Services. At The Business Research Company , he leads research operations across syndicated studies, customized consulting engagements, and the Global Market Model platform. His professional experience includes supporting organizations such as Boston Consulting Group, KPMG, and Ernst & Young. Wasay holds a degree in Electronics and Communications Engineering, postgraduate management qualifications from International Management Institute Belgium and Indian School of Business and Entrepreneurship, and completed the Integrated Program in Business Analytics from Indian Institute of Management Indore.